Library books can appear on your credit report. Your monthly cell phone bill usually does not. Neither does rent. Neither do utilities. Neither do groceries. Neither does the cost of staying alive. But a credit card does. A personal loan does. A car note does. Anything that charges interest does. That is not accidental.

The modern credit system was not designed to measure stability, reliability, or responsibility in everyday life. It was designed to measure something far more specific: how profitably you can be loaned to.

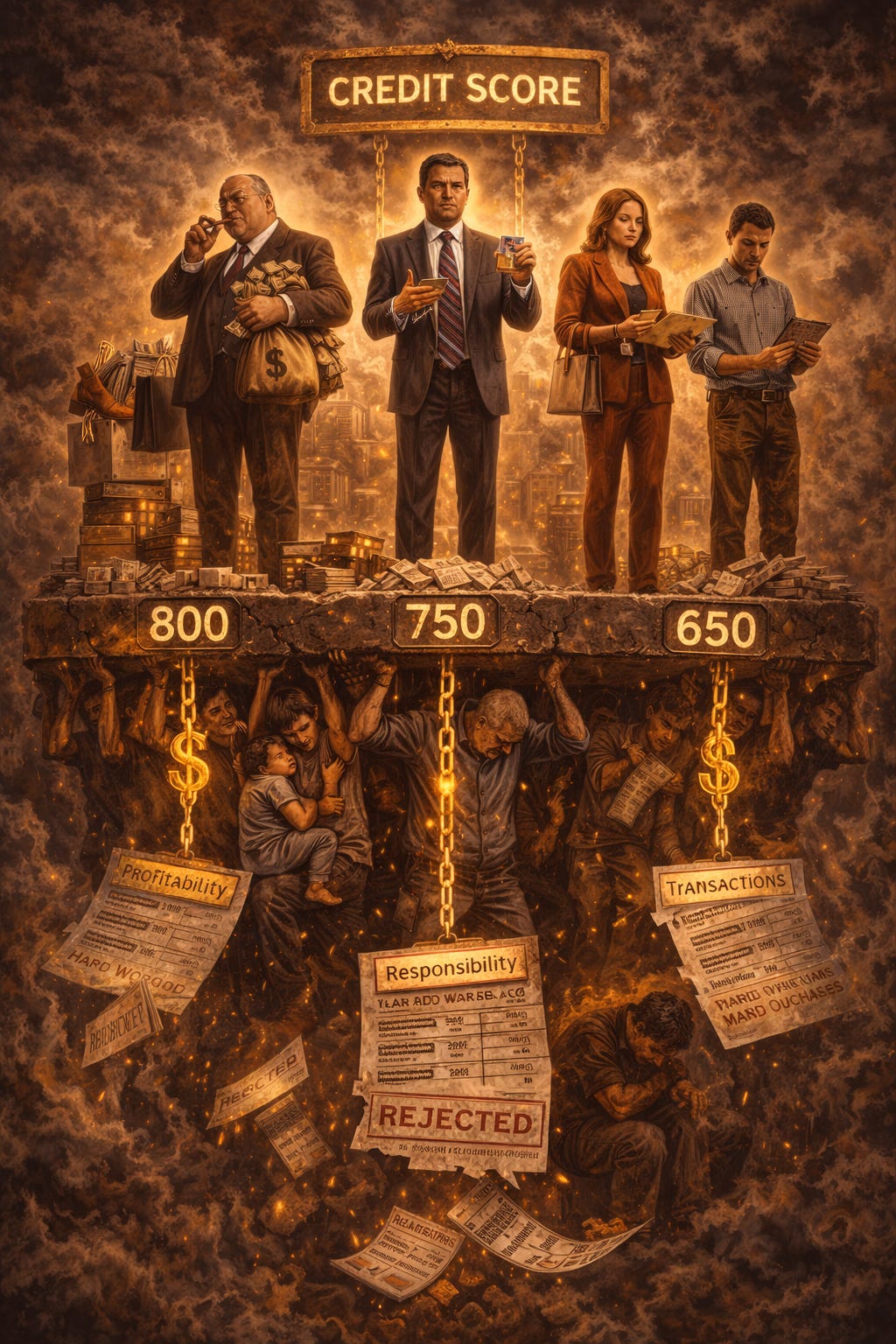

Housing often consumes roughly a third of household income, yet on-time rent payments were historically excluded from standard credit scoring models, while interest-bearing debt remained central.

If a payment does not generate interest, it largely does not count. You can pay rent on time for twenty years and be considered a risk. You can juggle debt for five years and be considered trustworthy. That alone tells you what the system is actually rewarding.

We are told credit scores reflect character. That they measure discipline. That they represent trust. In reality, they measure exposure. The more financial products you hold, the more data exists to track you. The more debt you carry, the more interest can be extracted. The more leverage you accept, the more valuable you become to lenders.

“Good credit” does not mean you are financially healthy. It means you are profitable.

There is a quiet absurdity here. In a world where identity theft is rampant, data breaches are routine, and financial fraud is constant, the people with the highest credit scores are often the most vulnerable. More open accounts. Higher limits. More points of attack.

Meanwhile, those with limited credit often carry less exposure. Fewer accounts to compromise. Lower financial risk surface. In a strange way, poor credit can function as protection. The system rewards openness to exploitation and punishes financial self-containment.

But the deeper problem is not irony. It is the loop. You need credit to access stability. Housing, transportation, and even employment increasingly depend on it. But you need stability to survive without credit. And the primary way to build credit is to take on debt.

Debt makes stability harder. So the system pushes people into borrowing in order to qualify for the very stability borrowing undermines. Round and round. We become the ouroboros, consuming ourselves to remain eligible.

Then comes the moral language.

When people struggle under this system, they are told it is about poor choices, irresponsibility, and a lack of discipline. But the system does not reward paying for necessities. It rewards participation in interest-bearing extraction. It does not ask whether you can feed yourself. It asks whether you can be charged. That is not a measure of character. It is a measure of profitability.

Credit scores now shape:

• housing access

• insurance rates

• job opportunities

• transportation costs

• interest burdens

All without democratic oversight. All through opaque formulas. All in service of private financial institutions.

A system built for lenders now governs everyday life. Responsibility has been redefined as willingness to participate in debt. The cruelest part is how normalized this has become.

People rarely question why rent does not count but revolving debt does. They simply accept that this is how adulthood works. But nothing about it is natural. It is a design choice. And like most design choices in modern capitalism, it shifts risk downward while extracting value upward.

We did not build a system that rewards stability. We built a system that rewards exposure. We did not measure whether people meet their obligations to live. We measured whether they generate revenue. And then we called it responsibility.

If a society truly cared about financial health, it would track:

• consistent housing payments

• utility reliability

• basic living costs met

• long-term stability

Instead, it tracks leverage. Because leverage is profitable. The credit system is not broken. It is doing exactly what it was designed to do.

The problem is that we allowed a profit metric to become a gatekeeper for human survival. And once you see that, the moral story collapses.

This was never about trust. It was about extraction.